The participation of people in the stock markets are increasing rapidly in India. In the past few years brokers across […]

Headline

Category: Finance

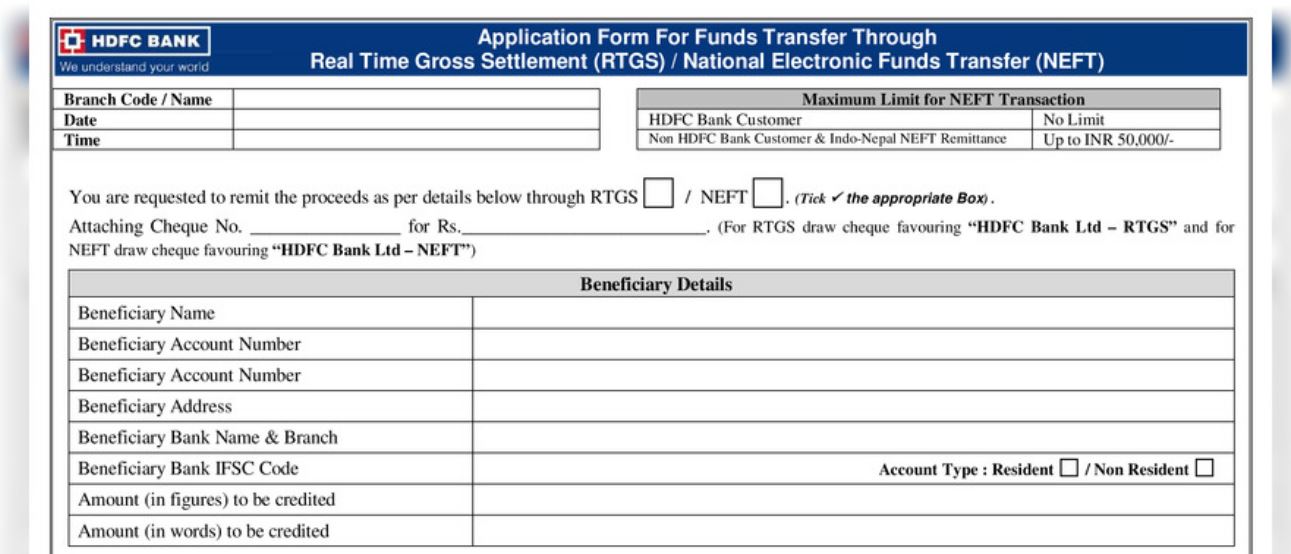

Download Now HDFC RTGS Form

HDFC RTGS Form is used for sending the amount overhead of Rs 2 lakh through any HDFC Bank Account. HDFC […]

What Does Public Liability Insurance Actually Cover?

If you’re a business, sole trader or are working as a contractor and have heard you need some kind of […]

Know the Benefits of Transferring a Home Loan

When you transfer your outstanding balance amount from your current lender to a new lending institution, it is known as […]

Online Payday Lenders

The main things you need to know about online payday lenders The interest rates on payday loans are often quite […]

How To Get Instant Loans: A Brief Overview

Instant Loans, I am sure by the name itself you can very well understand what I am talking about it […]

What is the GST Registration Process and What are It’s Requirements?

India in 2017 made a major indirect tax change, as goods and services tax was introduced. It subsumed almost every […]

Leading Multinational companies in India

Many top-notch and prestigious multinational companies reside in India. India is one of the most competitive nations across the world […]

Life Insurance for Children

Should you purchase life insurance for your children? Well, it’s a tricky question because typically life insurance is to protect […]

Medical Bill Income Tax Exemption and Steps to Claim It

In the recent past, the number of health issues and their treatment costs has gone up by leaps and bounds […]